Was auf dem Gelände tatsächlich geschieht und wie dort der Gewinn entsteht!

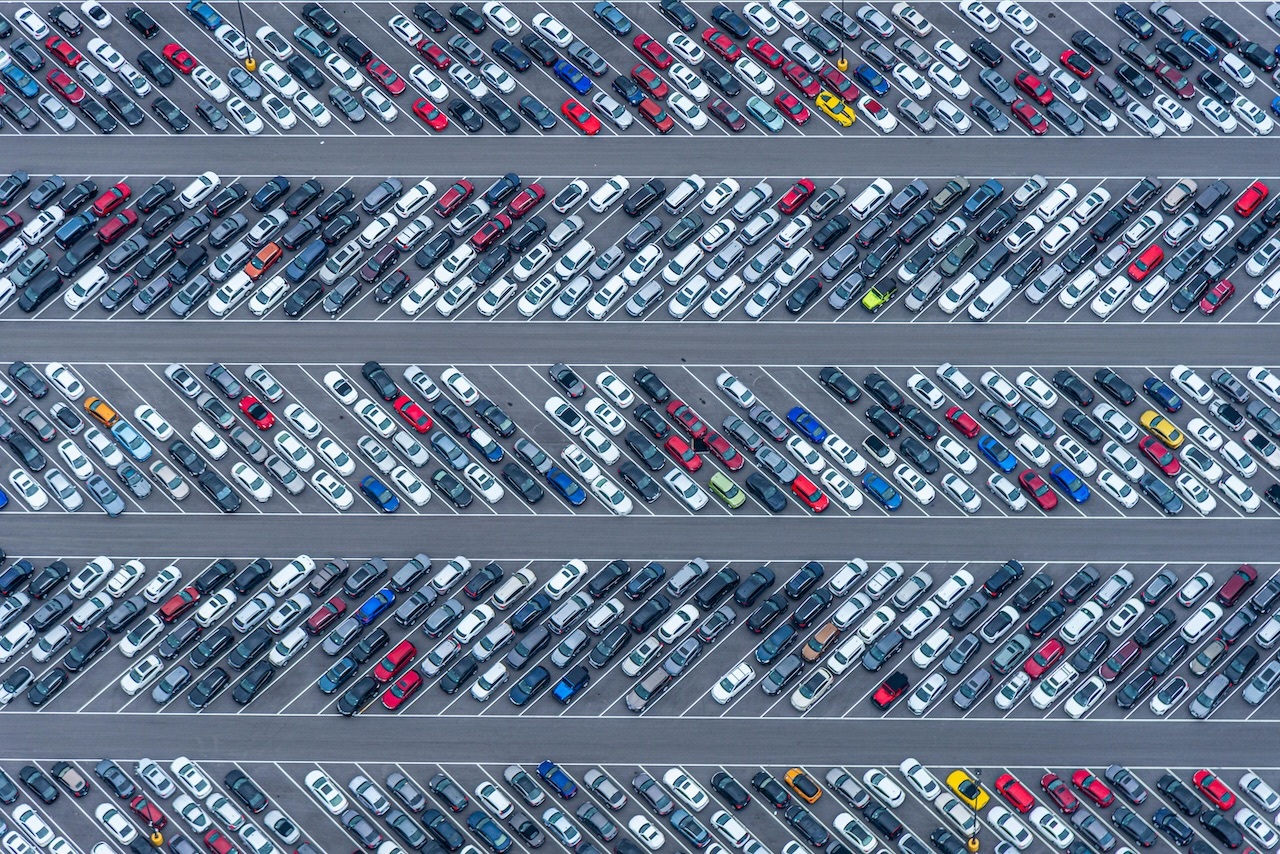

Wer täglich in der Autologistik arbeitet, kennt das Bild: weitläufige Gelände - bis zum Horizont gefüllt mit Autos, die scheinbar ungenutzt herumstehen. Für den zufälligen Passanten sind es Parkplätze. Für die Branche selbst bilden sie das Nervenzentrum einer Industrie, in der Timing, Wert und Information ständig neu austariert werden.

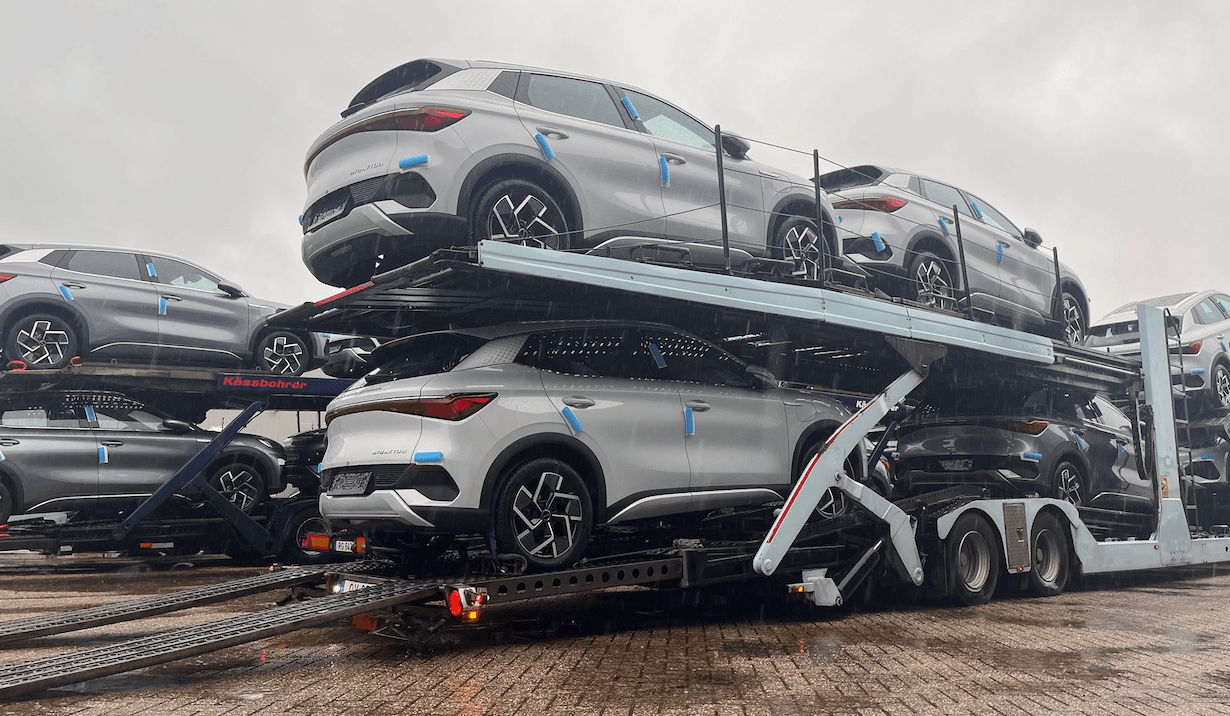

Diese Gelände – "Compounds" oder Fahrzeugverarbeitungszentren – sind kein Endpunkt, sondern eine Zwischenstation. Ein Ort, an dem Fahrzeuge nicht warten, sondern verwandelt werden: von eingegangener Ware in ein verkaufsfähiges Produkt. Und genau dort, in diesem scheinbaren Stillstand, entscheidet sich, wie viel ein Auto am Ende einbringt und wie schnell es seinen nächsten Besitzer erreicht.

Ein Markt, der größer ist als der Neuwagenverkauf

Wer glaubt, bei dieser Logistik gehe es vor allem um Neuwagen, betrachtet die falsche Seite des Marktes. In Europa werden jährlich Dutzende Millionen Gebrauchtwagen gehandelt. Das Volumen übersteigt das des Neuwagenverkaufs bei weitem.

| Merkmal | Wert |

|---|---|

| Jährliches Volumen (EU + UK) | ± 40 Millionen Fahrzeuge |

| Marktwert | ± 440 Milliarden Euro |

| Anteil an Gebrauchtwagen | ± 2/3 des Marktes |

Das macht den Compound nicht zu einem logistischen Detail, sondern zu einem strategischen Bindeglied. Denn während Neuwagen relativ vorhersehbar durch die Kette laufen, kommt ein Gebrauchtwagen als unbekannte Größe an: mit Verschleiß, Schäden, fehlenden Papieren oder einem unklaren Bestimmungsort.

Mehr Werkstatt als Parkplatz

Wer auf ein solches Gelände fährt, sieht vielleicht Reihen von Autos, übersieht aber, was dahinter geschieht. Jedes Fahrzeug durchläuft eine Reihe von Schritten, die gemeinsam darüber entscheiden, ob und wie es wieder auf den Markt kommen kann.

| Prozessschritt | Aktivitäten |

|---|---|

| Annahme | Registrierung, Inspektion |

| Technik | Reparatur, Aufarbeitung |

| Verwaltung | Dokumentenprüfung, Zoll |

| Verkaufsvorbereitung | Fotografie, Berichterstattung |

| Logistik | Planung, Transport |

Das Gelände ist damit ein Ort, an dem Logistik und Technik zusammentreffen. Hier wird nicht nur gelagert, sondern vor allem gearbeitet: an der Instandsetzung, an der Wertermittlung, am Vertrauen.

Warum ein Auto wochenlang stehen bleibt

Dennoch kann ein Auto, das innerhalb weniger Stunden bearbeitet werden könnte, wochenlang auf einem solchen Gelände stehen bleiben. Das erscheint ineffizient, ist aber meist die Folge einer Häufung kleiner Verzögerungen.

In der Praxis läuft es auf vier notwendige Freigaben hinaus, von denen jede für sich genommen zum Engpass werden kann.

| Freigabe | Grund für die Verzögerung |

|---|---|

| Technisch | Schäden, Defekte, leere Batterie |

| Dokumentarisch | Papiere, Inspektionen, Zoll |

| Kapazität | Transportengpässe, Ladeanschlüsse |

| Standort | Fahrzeug schwer auffindbar |

Selten ist es ein einzelnes Problem, das ein Auto aufhält. Es ist die Kombination verschiedener Faktoren – ein fehlendes Dokument, eine volle Werkstatt, ein verpasster Transporttermin –, die die Durchlaufzeit verlängert.

Ursachen für Verzögerungen

Wer sich die Praxis ansieht, erkennt Muster. Manche Ursachen treten immer wieder auf und belasten die Durchlaufzeit strukturell.

| # | Faktor | Auswirkung |

|---|---|---|

| 1 | Warten auf Entscheidung des Eigentümers | 2–6 Wochen |

| 2 | Dokumente & Prüfung | Tage–Wochen |

| 3 | Transportkapazität | 1–3 Wochen |

| 4 | Aufbereitungskapazität | 1–3 Wochen |

| 5 | Technische Probleme | Variabel |

| 6 | Fahrzeug nicht auffindbar | Stunden–Tage |

| 7 | Schlüssel / Software | Tage |

| 8 | Leere 12-V-Batterie | Sehr häufig |

| 9 | Ladezustand des Elektrofahrzeugs | Zunehmend |

| 10 | Witterungseinflüsse | Gelegentlich stark |

Auffällig ist, dass die größten Verzögerungen oft nicht physischer, sondern organisatorischer Natur sind: das Warten auf eine Entscheidung, auf ein Dokument oder auf den den nächsten Schritt in der Lieferkette.

Compounds an strategischen Standorten

Die größten Compounds befinden sich nicht zufällig dort, wo sie liegen. Sie gruppieren sich um Häfen, Eisenbahnlinien und logistische Knotenpunkte – Orte, an denen internationale Ströme zusammenlaufen.

| Region | Rolle | Wichtige Akteure |

|---|---|---|

| Antwerpen–Zeebrügge | Größter Knotenpunkt weltweit | ICO, Mosolf |

| Bremerhaven | Deutscher Exportmotor | BLG |

| Frankreich (Le Havre) | Mittelmeer | CEVA |

| Spanien (Barcelona) | Südeuropa | Grimaldi |

| Mitteleuropa | Wachstum bei Gebrauchtwagen | Lagermax |

| NL/DE-Korridor | Hinterlandanbindung | Koopman |

Hier wird deutlich, dass das Gelände nicht nur ein lokaler Standort ist, sondern Teil einer kontinentalen Infrastruktur.

Effizienz versus Risiko

Der Nutzen von Compounds liegt auf der Hand: Sie bringen Ordnung in einen chaotischen Strom. Gleichzeitig fügen sie der Kette eine zusätzliche Ebene hinzu.

| Vorteil | Wirkung |

|---|---|

| Pufferfunktion | Geringere Abhängigkeit vom Timing |

| Zentralisierung | Effizienterer Transport |

| Standardisierung | Weniger Diskussionen über Schäden |

| Nachteil | Auswirkung |

|---|---|

| Zusätzliche Instanz | Höheres Schadensrisiko |

| Lagerung im Freien | Wetterrisiken |

| Komplexität | Risiko von Ineffizienz |

Die Frage ist also nicht, ob Compounds notwendig sind, sondern wie gut sie gesteuert werden. Darin liegt der Unterschied zwischen Gewinn und Verlust.

Das Elektroauto und die Compounds

Der Vormarsch der Elektrofahrzeuge verändert die Spielregeln grundlegend. Was einst vor allem ein logistisches Problem war, wird zunehmend zu einem technischen und energetischen Problem.

| Thema | Auswirkungen |

|---|---|

| Sicherheit | Strengere Vorschriften, separate Zonen |

| Laden | Neue Kernaktivität |

| Gewicht | Weniger Autos pro Transporter |

| Daten | Der Zustand der Batterie wird entscheidend |

Ein Elektroauto, das zu lange stillsteht, verliert nicht nur Zeit, sondern auch nutzbare Energie. Das Laden wird damit nicht zur Nebensache, sondern zu einem integralen Bestandteil des Prozesses.

Wo der wahre Gewinn liegt

Der Reflex in der Branche ist oft, in mehr Kapazität zu investieren: mehr Gelände, mehr Lastwagen, mehr Infrastruktur. Doch der größte Gewinn liegt offenbar woanders: in Koordination und Information.

| Lösung | Auswirkung |

|---|---|

| Daten vor der Ankunft | Kürzere Wartezeiten |

| E-Gates & Slots | Weniger Staus |

| KI-Inspektion | Schnellere Berichterstattung |

| Yard-Automatisierung | Weniger Suchaufwand |

| EV-Betriebsmodell | Effizienteres Beladen |

| KPIs nach Ursache | Mehr Transparenz |

Der Umschlagplatz der Zukunft ist daher weniger ein bloßer physischer Ort als vielmehr ein digitaler Knotenpunkt.

Vom Parkplatz zum Kontrollraum

Was einst als praktische Lösung begann – ein Ort, an dem Autos vorübergehend abgestellt werden konnten –, hat sich zu einem strategischen Instrument entwickelt.

Hier entscheidet sich, wie schnell sich ein Fahrzeug durch die Lieferkette bewegt, wie viel Wert es behält und wie viel Marge übrig bleibt. In einem Markt, der immer internationaler, digitaler und komplexer wird, verlagert sich die Macht auf jene Akteure, die diese Zwischenphase im Griff haben.

Nicht unbedingt die größten Flächen gewinnen. Die Gewinner sind diejenigen, die Informationen, Prozesse und Logistik am besten aufeinander abstimmen.

Was für die Außenwelt ein Feld mit stehenden Autos bleibt, ist in Wirklichkeit ein Ort, an dem alles in Bewegung ist.